Now Frugal Man Needs a Budget as Retirement Approaches

I stumbled upon one of those online calculators the other day. It’s the one that shows you how well you’re budgeting money for retirement savings, and it returned some distressing news.

After 37 years in the workforce, I am 33 percent of the way toward what I need to retire.

Really? Yes, really.

I have been working full-time since I was 21, and as The Most Frugal Man in America, I’ve been prudent with my money my whole life. I have successfully dealt with student loans, home loans and car loans. I have been conscious of the need for retirement savings my whole work life.

I also have been married 24 years, raised three sons — two in college and one about to go there — and that combination leaves me unconscious at times.

I could have avoided this savings shortage if I had budgeted for retirement, but that would have required me having a budget in the first place. That has never happened. Not once in my 58 years have I predicted or recorded the money coming in or going out. I have zero records showing how much it cost to get a wife and kids, and how Frugal Man fell 67 percent short of where he needs to be as retirement approaches.

I now have seven to eight years to fill that 67 percent gap, while also juggling continuing obligations for home, cars and college, as well as the insurance, maintenance and taxes that go along with them.

This feels like a good time to start a budget.

The Budgetnista Will Help

Fortunately, I found someone to guide me through the process. Her name is Tiffany Aliche. She has a catchy moniker, “The Budgetnista,” which is not only memorable, but appropriate for the problem.

She dealt with her first budget at the age of 11. She has a bachelor’s in finance and a master’s in education. She’s been a financial consultant for six years, and her thoughts on budgeting appear in publications like Forbes, USA Today and The Huffington Post. She also wrote a book called “The One Week Budget” and has appeared on several network programs, including the “Today” show.

That more than qualifies her to counsel a 58-year-old rookie on how to start budgeting.

“Age doesn’t matter,” Aliche said. “Budgets are a plan for your money so if you’ve got money — no matter how old you are — I can help you make a plan for it.”

I do need a plan, but then again, so does most of America. A 2012 Gallup survey shows that 68 percent of Americans don’t have a budget. We wing it and hope for the best.

“Bad move,” Aliche said. “People think budgets are a tool to tell you what you can’t do with your money. That’s wrong! Budgets are a tool to tell you what you can do with the money you have.”

Why Is Budgeting Like Work?

The problem then is how to do this without making it a part-time job. Budgeting appears to involve far more time and frustration than it’s worth. That is the main reason I don’t budget, and I’d bet that’s why 68 percent of America doesn’t either.

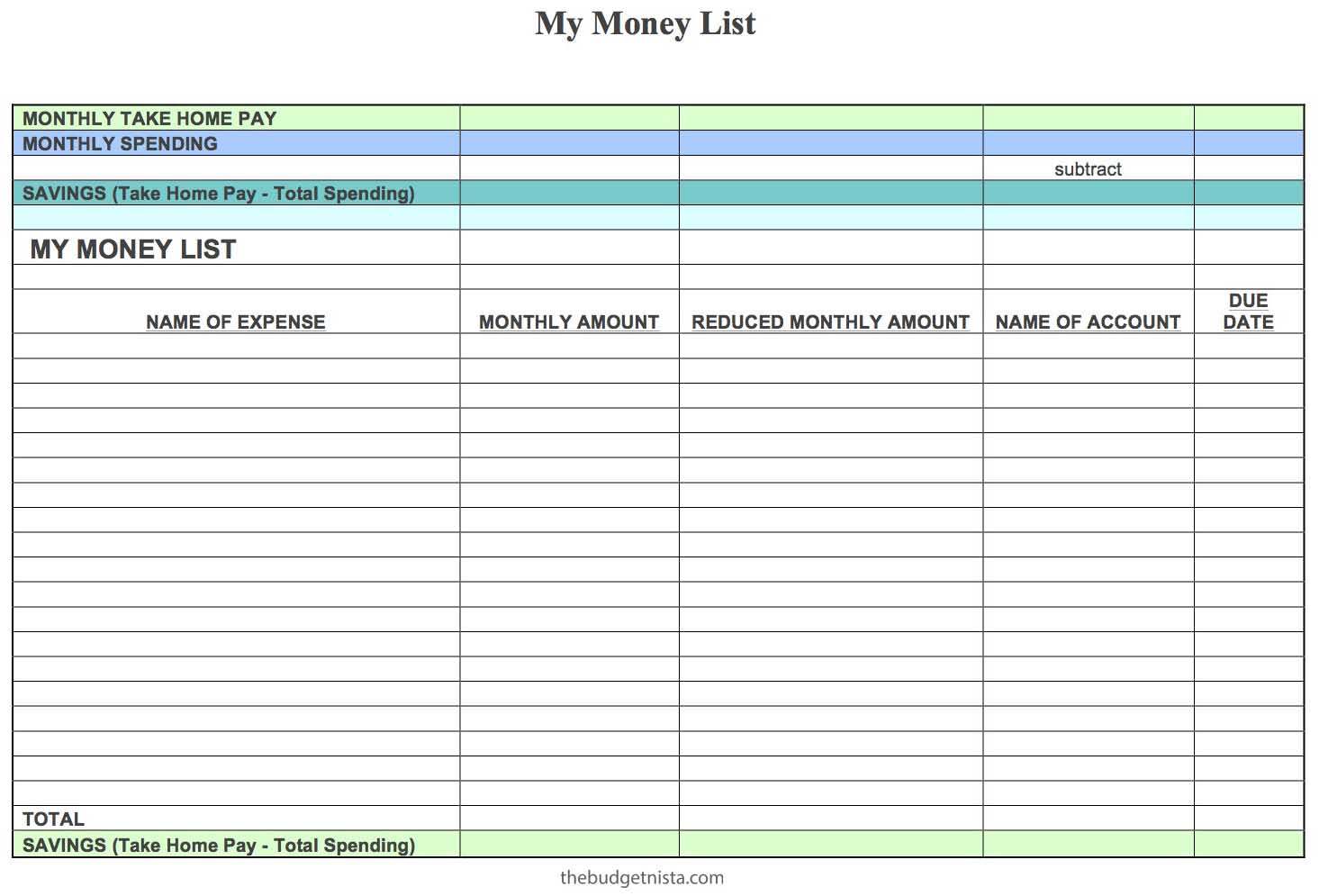

Aliche says budgeting will be like a job, but only for about half a day. That’s how long she says it takes to get through the first part of the three-step organizing process she calls “The Money List.” It works like this:

- List everything you spend money on. I repeat: Everything. Don’t worry about how much you spend, just list every item you spend money on.

- Calculate how much money you spend monthly on each item. For example, if you get your car serviced every three months and that maintenance runs about $100, then put $33.33 ($100/3 months) for the monthly spending. If you pay $300 for an annual gym membership, put $25 ($300/12 months) for the monthly spending.

- Add the monthly spending and subtract it from your “take home” income. That’s the net amount you receive for your job or jobs, if you get paid by more than one employer.

The remainder is what you put into your savings fund, vacation fund, home improvement fund or, in my case, retirement fund.

But will this fill in the 67 percent gap?

“Give it a few months, and then we’ll take a look at how you’re doing,” Aliche said. “The Money List won’t lie. You’ll have an honest picture of what you’re doing with your money. If you’re not saving enough for retirement, we’ll make a plan to make that happen.”

Fair enough. We’ll check in with the Budgetnista — and that online retirement calculator — in six months and see where we’re headed.