Home > Debt Help Advice >

What do you call it when someone tells one side of a story?

Dave Ramsey calls it: “The Truth.”

Ramsey boldly proclaims on DaveRamsey.com that he’s going to deliver “The Truth About Debt Consolidation,” and instead, serves up a one-sided batch of glittering generalities, half-truths and flat-out untruths that have zero foundation to support them.

Let’s review Dave Ramsey’s bad math claims: “You end up paying more and staying in debt longer because of so-called consolidation. Get the facts before you consolidate.”

Just don’t get them from Dave. He doesn’t have any. He offers nothing to substantiate that premise. No data, no stats, no surveys, no government, college or industry research to prove his claim that you pay more and stay in debt longer by consolidating.

What he does offer is chance to buy an online version of “The Truth” for $119.

We don’t fault him for trying to make a buck, but if you’re peddling “The Truth” most people want the whole truth.

Not half … at least not for $119.

The Truth About Debt Consolidation

The truth about Dave Ramsey’s “The Truth About Debt Consolidation” is that there is so little truth in it, you wonder how his conscience doesn’t bother him.

The guy is supposed to be a financial guru and he can’t even do the simple math on what it would cost to get a debt consolidation loan.

Dave devotes an entire section of his truth about debt consolidation page to “How Does Debt Consolidation Really Work?” and botches the math so badly you wonder if his calculator needs batteries.

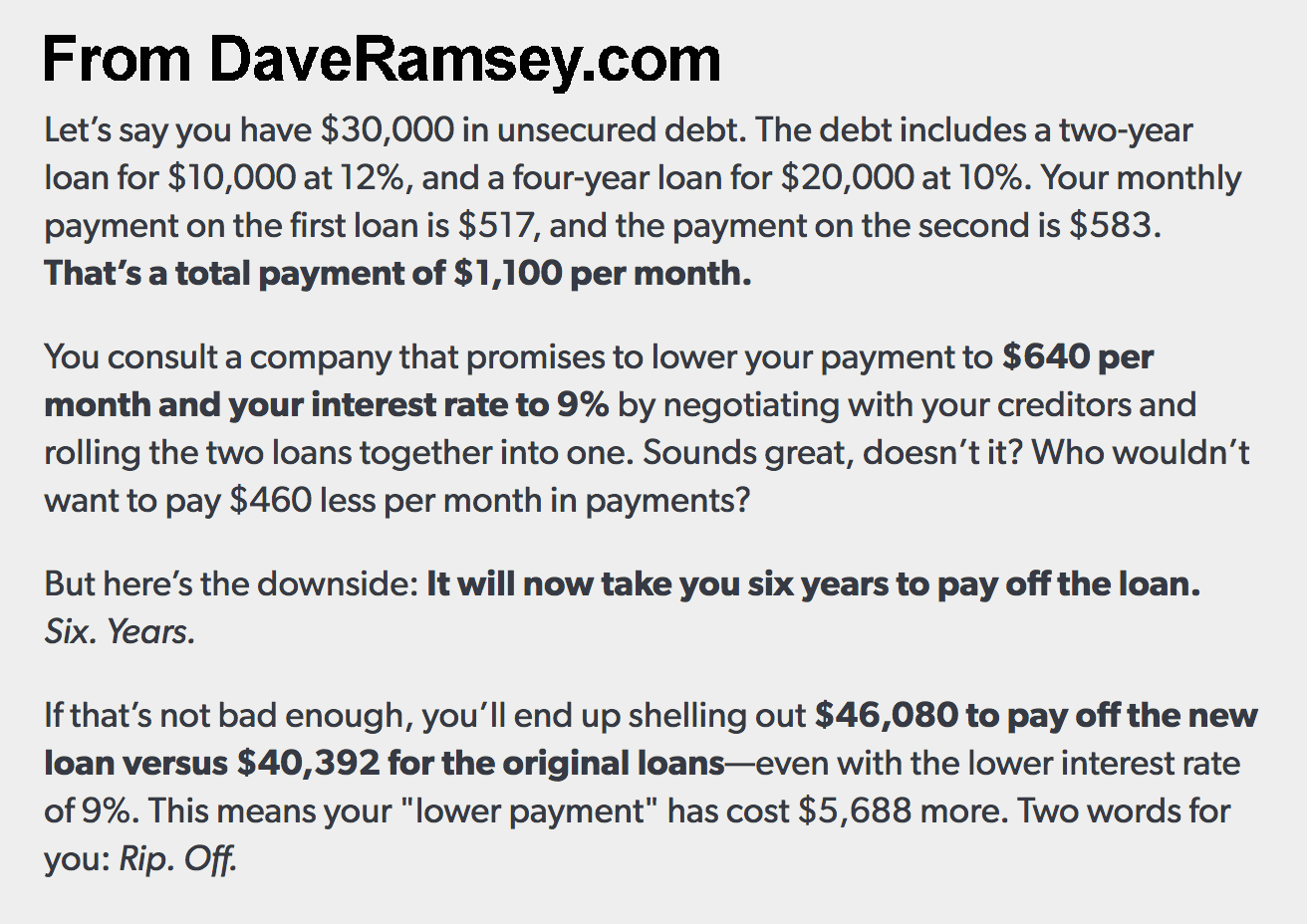

Dave starts with an example of someone with $30,000 in unsecured debt and then does the math to try and prove his point that consolidation doesn’t work.

Only his calculator misfires on him. Completely misfires. Misses by thousands of dollars and his “truth” turns out to be a numeric lie.

According to Dave, if you have a two-year loan at 12% on $10,000 of the debt, you pay $517 a month. You really pay $471. He’s off by $46 a month.

According to Dave, if you have a four-year loan at 10% on the other $20,000 of debt, you pay $583 a month. You really pay $507. He’s off by $76 a month.

And according to Dave, if you got a $30,000 debt consolidation loan at 9% for 72 months, you’d be paying $640 a month. You really pay $540. He’s off by $100 a month.

Dave concludes that the total cost for the original loan would have been $40,392 and the consolidated loan would have cost $46,080, a difference of $5,688, which is substantial.

But is also, not true.

The real truth is that the original loan would have cost $35,646 and the consolidated loan would have cost $38,935, a difference of $3,289.

However, if you consolidated your $30,000 debt at 9% on a four-year loan, your total payments would be $35,786, or about $140 difference from what you would have paid on the original loan. That is not substantial.

But it is true.

Do you really want financial advice from a guy who can’t do simple math?

Two words for you Dave: New. Calculator.

The Real Truth About Debt Consolidation

To be fair, Dave is right on one point: No matter how you do the math, paying off a loan in six years, costs more than paying one off in two years. That is one of the few true truths he espouses on debt consolidation.

Most of his assertions on “The Truth About Debt Consolidation” are casual observations not data-driven conclusions.

There is a page full of misconceptions, but rather than go into detail, let’s highlight the biggest blunders.

- Debt management programs are completely left out of the discussion on debt consolidation. That is like leaving LeBron James out of the discussion for Most Valuable Player in the NBA. Why have the discussion if you’re not going to include a major player? Debt management consolidates your credit card debt; works with card companies to reduce interest rates and monthly payments to an affordable level; and eliminates debt in somewhere close to three years. Debt management programs consolidated debts for 250,000 people last year and 100,000 new consumers sign up every year to replace the 100,000 who leave after paying off their debt.

- Another of Dave assertions –“Debt consolidation is the combination of several unsecured debts like payday loans, credit cards, medical bills into one monthly bill.” – is barely even half right. Debt consolidation does combine several unsecured debts, but those debts are almost all just credit cards. It’s rare to virtually impossible that someone who is behind on a payday loan is going to have a bank approve them for a debt consolidation loan.

- Dave says: “Debt consolidation promises one thing but delivers another.” What does it deliver Dave? He never says what it delivers, though it’s not a big secret. If you make on-time payments in a debt consolidation plan, it promises to eliminate your debt, just like any other debt-relief program.

- Dave says that “Dishonest companies that promote too-good-to-be-true debt relief programs continue to rank as the top consumer complaint received by the Federal Trade Commission.” The FTC said in a Mar. 1, 2018 report that it’s top complaint was for debt collection agencies with identity theft second and imposter scams third. Debt-relief companies were not listed in the Top 30 categories released by the FTC.

- Dave says: “When you consolidate, there’s no guarantee your interest rate will be lower.” Another half-truth. Debt management programs only work if you qualify for a lower interest rate on your debt. If you don’t qualify for a lower interest rate, why would you join the program? So Dave is half-right. There is no guarantee, but if you don’t like the interest rate being offered, you can decline. That’s a guarantee.

Dave would have you believe that the debt snowball is the only game in town. It’s not.

Let’s end on a fair note because even though Dave is spreading more half-truths and quarter-truths than real truths, he does mean well and he’s right about one thing:

“The solution isn’t a quick fix … The solution requires you to roll up your sleeves, make a plan for your money and take action!”

Debt management programs could be part of that action. So could debt consolidation loans and debt settlement. It’s up to consumers to do some research and see what type of debt consolidation fits your lifestyle.

That is the truth about debt consolidation.

As for Dave Ramsey’s version of “The Truth About Debt Consolidation” … he might want to change the title to something more appropriate like: “The Partial Truth About Debt Consolidation.”

Oh, and get some batteries for that calculator!

Read our analysis of the Dave Ramsey budget.

Sources:

- NA, ND. The Truth About Debt Consolidation. Retrieved from https://www.daveramsey.com/blog/debt-consolidation-truth

- NA. (2018, March 1) Consumer Sentinel Network Data Book 2017: Report Categories. Retrieved from https://www.ftc.gov/policy/reports/policy-reports/commission-staff-reports/consumer-sentinel-network-data-book-2017/report-categories