Is Debt Affecting our Economic Freedom?

As we approach July 4, the 237th anniversary of our nation’s independence, it’s also worth noting that our country is in its fourth year of a sluggish recovery from the Great Recession — our most severe economic contraction in generations.

So even as we celebrate America’s freedoms — and especially the economic advantages we all enjoy — we should also take stock of the system’s built-in limitations and challenges.

While our national economy has made some positive gains over the past few years, most tellingly in the areas of corporate profits, housing prices and a rising stock market, it is just as true that many fellow Americans have not shared in those achievements, nor recovered lost wealth, homes, jobs or opportunities for future advancement.

When taking stock of America’s fiscal health, it’s a good time to see how the two main categories of debt — personal and national— affect our daily lives, economic freedom, and ability to prosper and grow as individual citizens and a nation.

Personal Debt

First let’s look at personal debt. Personal debt can hinder one’s actual freedom (ask someone who can’t afford a lawyer), but mostly it constrains one’s economic freedom, especially if there is too much of it.

And today, many Americans are heavily in debt.

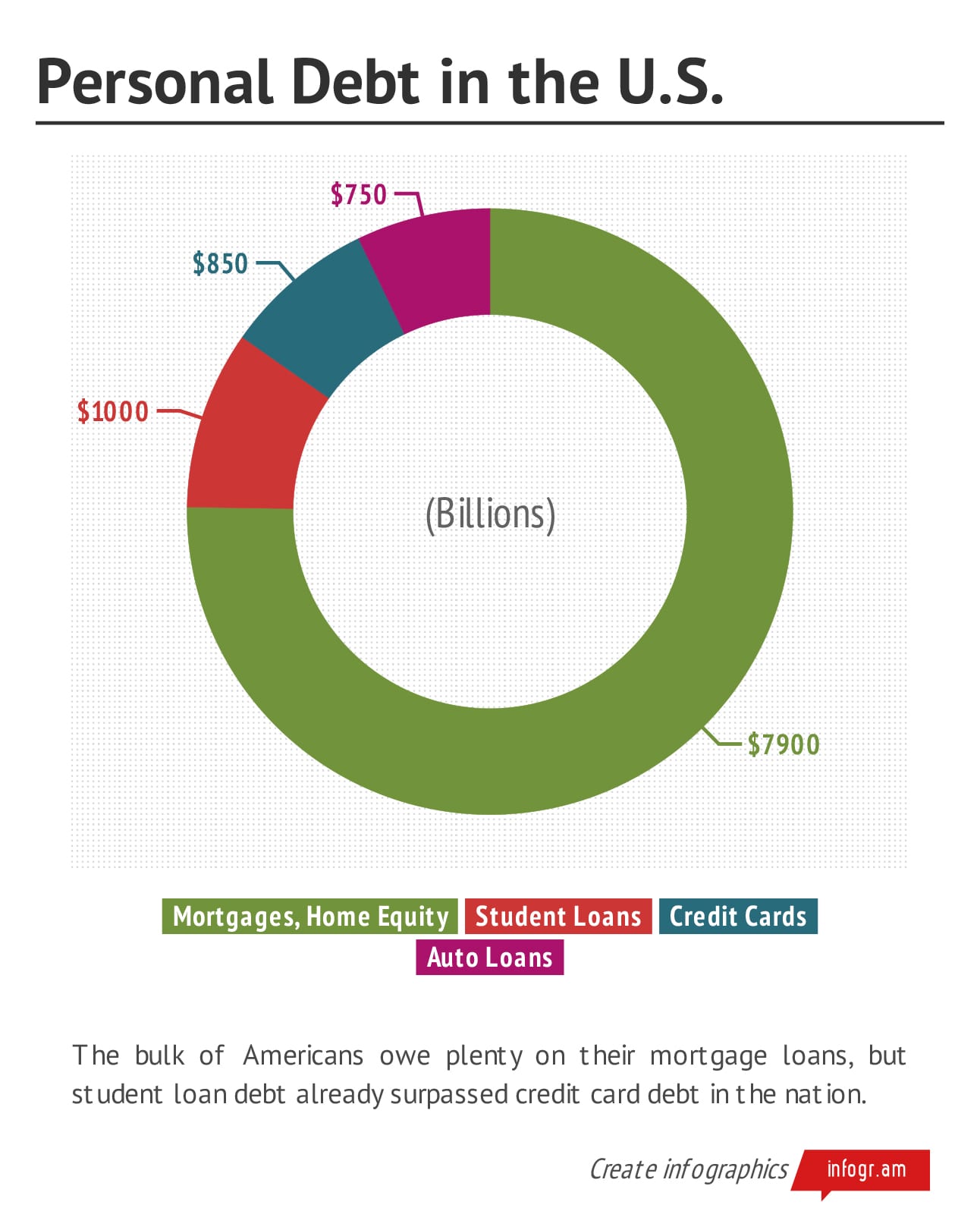

Here’s a breakdown of personal debt stemming from mortgages, home equity, student loans, credit cards and other high-debt items.

Student loan debt in the nation, which reached $1 trillion in 2012, surpassed the $850 billion debt stemming from credit cards for the first time.

For many Americans, the monthly mortgage payment takes the greatest slice out of their budget. With the collapse of the housing market five years ago, many homeowners found themselves “underwater” – meaning that they owed more on their mortgages than their homes were worth. Some 10.8 million homes, or 22 percent of all mortgages in the country, are currently underwater.

These homeowners are much more likely to default on their loans and are less able to refinance at today’s lower rates, which, if they could, would help them reduce their monthly mortgage costs. In addition, many of these underwater home owners who are still unemployed cannot sell their homes in order to move where they might find jobs. Clearly their economic freedom is being compromised since they are tethered to underwater homes and expensive mortgage payments.

The growing student loan debt is also crippling many of our young Americans as they leave college. Students who borrowed money and have just graduated in the Class of 2013 will exit school with more than $32,000 in debt. That number is destined to rise by thousands of dollars and affect a quarter of all new student borrowers, unless Congress acts to minimize or reverse the recent doubling of interest rates on the federal government’s subsidized Stafford Loan program.

The consequence: Former students are not buying as many cars or homes as previous generations were able to. Their economic freedom, therefore, is compromised severely by their heavy student debt load.

Credit cards and automobile loans generally charge higher interest rates than all other categories of borrowing. In addition, penalties and late fees can add to a borrower’s overall debt burden, making it more difficult pay off balances and stay out of the red.

Most people who seek the help of debt relief companies do so because they have trapped themselves in credit card debt and can’t climb out. Statistics show the average American household carries about $15,590 in credit card debt.

When the federal government needs money to pay its bills, it can borrow the money, raise it through taxation or increase the money supply by putting more currency directly into circulation. But when you and I need money, our options are more limited: Get a better paying job, sell material assets, borrow even more from willing lenders or win the lottery.

In most cases, though, we must make difficult choices between what bills to pay and what cannot be paid for. A budget can help show how much money is coming in and how it’s spent.

The National Debt

The national debt is money the federal government owes to its combined creditors. It’s a subject much discussed lately in the daily media, the halls of Congress, and in homes and businesses across the country.

The official debt of the United States government, as of June 1, stands at more than $16.7 trillion. Census figures show the U.S. population is inching past 316 million.

That means our total debt amounts to nearly $53,000 for every person in the nation or roughly $145,200 per American household.

The national debt can be broken down into two parts: The majority of it, nearly $11.9 trillion, is owned by the public in marketable U.S. Treasury bills, notes and bonds as well as in various non-marketable financial instruments. The remaining $4.84 trillion is money the federal government owes to itself in intra-governmental holdings, such as the Social Security Trust Fund.

Regardless of how it is sliced, $16.7 trillion is a lot of red ink.

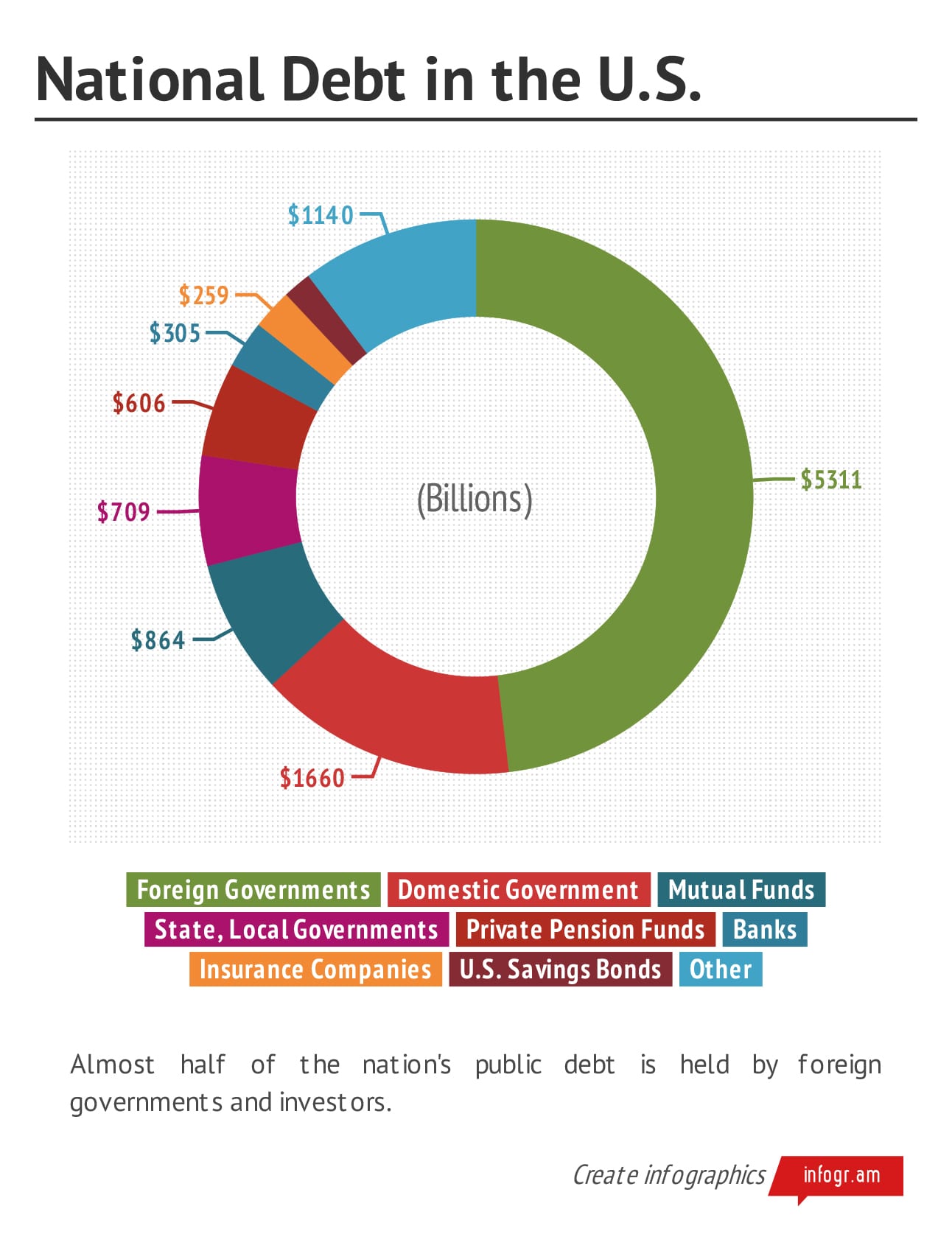

Here’s a breakdown of some of the national debt that is held by foreign governments (which amounts to almost half of the owned debt), domestic entities like the Federal Reserve and state and local governments, and other institutional investors.

More than a quarter of the national debt is held by foreign, domestic, and state and local governments, as well as mutual funds.

While some economists believe that the national debt, as big as it is, is not an immediate worry – historically, the nation has always been in debt, even in times of robust growth – many of the country’s elected leaders have used the size of the debt to constrain government spending on policies important to millions of Americans.

Thus, the current political reality has resulted in reduced spending on infrastructure, job creation, unemployment benefits, aid to poor children, and many other programs that might expand the overall economy and therefore extend the bounties of financial freedom to many more individuals and families.

Is Debt Limiting Our Freedom?

To sum up: Our national debt can be problematic, but history shows that a high national debt is not necessarily detrimental to our country’s economic freedom, unless the fear of it reinforces the notion that spending on important programs and policies needs to be restrained.

Likewise, personal debt, when managed well, can actually promote personal economic freedom because it allows borrowers to spend money they don’t currently have for important reasons like buying a home, a car, or going to college.

However, high or unmanageable debt is almost always a detriment to one’s personal economic freedom, because it limits choices, and constricts one’s ability to accumulate wealth and plan for the future.

There is little we can do as individuals to influence the size of our national debt, but we can certainly exercise some control over our personal ones.

While celebrating our country’s freedom, this July 4, we should also continue to strive to free ourselves from onerous debt and burdensome financial obligations.